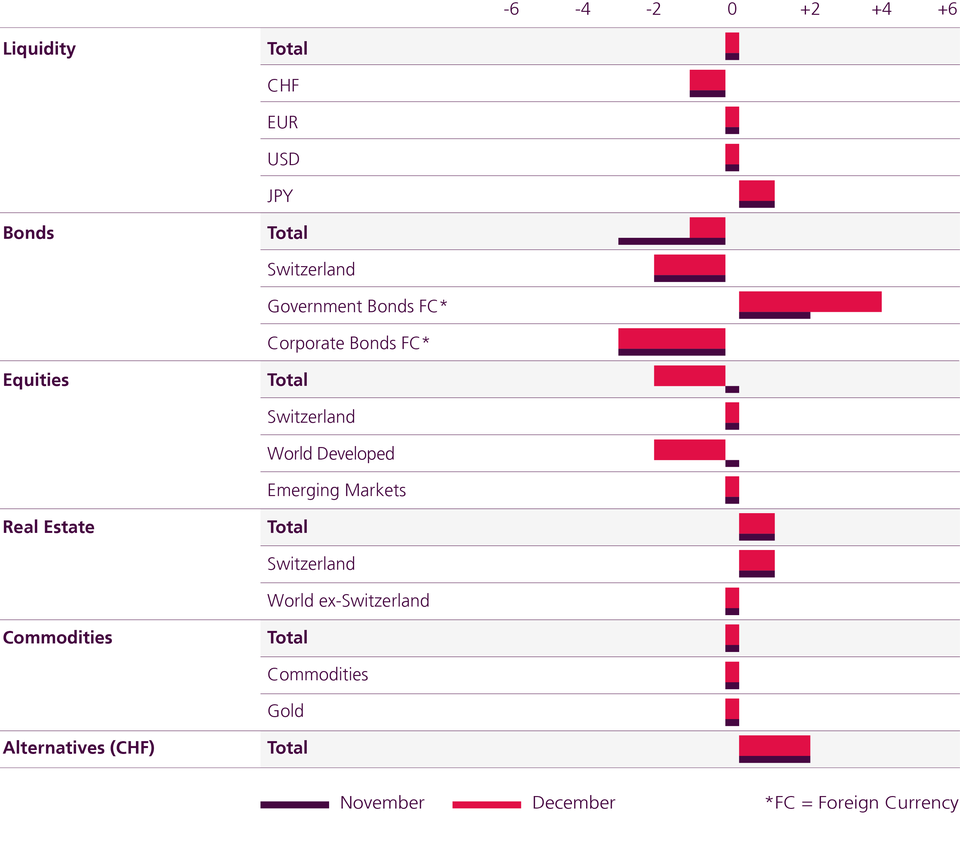

These are our reasons for reducing the equity quota:

- We believe that the hopes for a less restrictive monetary policy by the Fed from 14 December are premature.

- The increase in equity markets still lacks breadth, so it is likely to fail on the moving 200-day average in line with the two bear market rallies in March and July/August.

- The earnings estimates priced in by the market are too high at around 8% for 2023 and need to be reduced in the coming weeks or months, maybe to zero earnings growth.

With the price increase of the last two months, the momentum of investments with risk premiums such as equities and high-yield bonds has improved significantly. What's more, December exhibits historically strong seasonality, and inflation will continue to fall according to our forecasts, especially in the USA – from the current 7.7% to below 4% in 12 months. If, according to our estimates, the global economy weakens only mildly (global GDP in 2023: +1.6% after +2.9% in 2022), these are reasonable prospects for 2023. Growth for Switzerland is forecast at +1.0% after +2.5%.