It is surprising how reliably the stock market indicator of "seasonality" has again worked during September. We had warned about the seasonally weak equity months of August and September and indeed the equity markets lost another 12%. Of course, this was not only due to seasonality. The fundamental trigger for the correction was a steady rise in bond yields due to the continued surprisingly high inflation figures, for example in the US with 8.3% and 6.3% core inflation. In the UK, the new government is torpedoing the monetary tightening of the Bank of England with tax cuts.

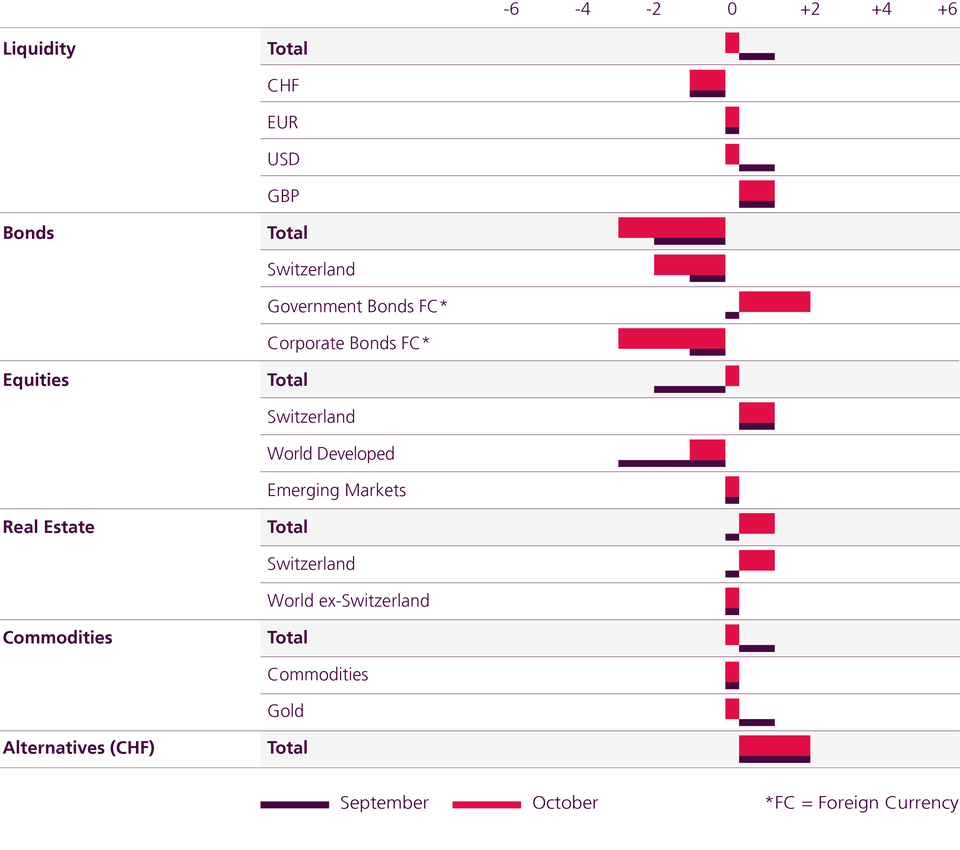

We are increasing our underweight in corporate bonds because we consider the current spread levels, for example the 150 basis points in USD investment grade, and the associated implicit default rates to be too low in view of the increased recession risks. Last month, our equity underweight was justified on the basis that we had rated notions of interest rate cuts and high earnings expectations as unrealistic. We were right to do so. Today, significantly higher key interest rates and no interest rate cuts are expected; earnings expectations have been revised downwards slightly. In addition, as equity markets are now oversold with a relative strength index at 24 and less than 5% of US equities are trading above their 50-day average, we are closing our equity underweight.