CoCo bonds – an asset class celebrates its 10th birthday

Contingent convertible bonds, or CoCos for short, are subordinated bonds typically issued by major European banks. Following the financial crisis, CoCos established themselves as an attractive means for banks to meet the regulator’s new capital requirements. The first CoCo issues came onto the market a good ten years ago.

Text: Maurizio Pedrini, Daniel Björk

We recognised the unique characteristics of this new asset class at an early stage and launched the first CoCo fund on the market as early as June 2011, providing investors with diversified access to this new asset class. Much has happened since its launch ten years ago; the asset class has successfully passed an extraordinary stress test most recently in the context of the coronavirus crisis. Together with our CoCo experts Daniel Björk and Maurizio Pedrini, we now reflect on ten years of CoCo bonds and look ahead to the future of the banking sector.

Mr Björk, you have been managing CoCo bonds for ten years – looking back at this time, what was the most turbulent period for CoCo investors and why?

Daniel Björk: The coronavirus crisis was undoubtedly the most turbulent time for CoCo investors. It was the first serious stress test for the banking sector since the Lehman crisis in 2008 and 2009. The systematic lockdowns worldwide were absolutely unprecedented. Nothing like them had ever been seen before this crisis. The sudden halt of societal life and financial markets led to enormous uncertainty, not least due to the central role of the banking sector. The combination of rapid and extensive fiscal and monetary policy measures, as well as the good profitability and solvency of the banking sector, helped to bridge the gaps created by the lockdowns. To date, the banks have weathered the crisis relatively well, as they are both profitable and have record capitalisation.

If we reflect on the development of the CoCo market, what developments would you have expected and where were you rather surprised?

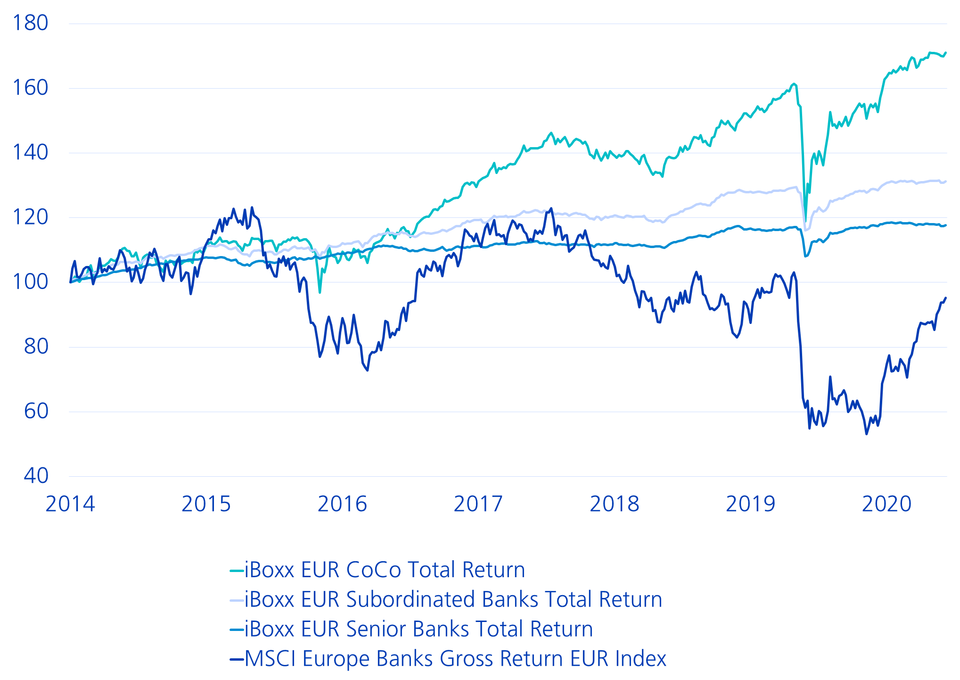

Daniel Björk: We would not have expected the outstanding performance of the CoCo market to this extent – especially compared to the development of the rest of the bank capital structure (equity, senior and subordinated bank bonds, see chart). That was definitely a highlight. Our main argument for CoCo bonds when launching our fund was our assumption or expectation that the higher capitalisation as a result of Basel III regulations would reduce investment risks for CoCo investors. The higher costs of capital due to Basel III caused additional costs for shareholders, as less capital was available for dividends and share buybacks. In summary: we expected good performance for CoCo bonds. However, we were surprised by the strong relative performance of CoCos compared to bank equities. CoCo bonds performed exceptionally well, while many bank equities have struggled in the last ten years (see chart).

CoCo performance compared to senior and subordinated bank bonds and bank equities

Mr Pedrini, where do you see future challenges and opportunities for the banking sector?

Maurizio Pedrini: Two mega-trends that are already a reality today and will continue to keep the banking sector busy for years to come are ongoing digitalisation and the increased focus on sustainability issues. We believe that those banks that are already strongly positioned today and have diversified business models can best master the challenges and benefit accordingly. However, this also requires investments in digitalisation and innovation, so that new business models can emerge.