What a start to the year!

The stock markets got off to a strong start at the beginning of 2023. In our Market Outlook, we had envisioned a return of around 5% for a mixed Swiss portfolio – for 2023 as a whole. This target of 5% was already achieved in January.

Stefano Zoffoli, Chief Strategist

- warm temperatures, with the positive effect that the energy crisis and recession in Europe are turning out to be modest,

- sharply falling inflation rates and

- the reopening of China.

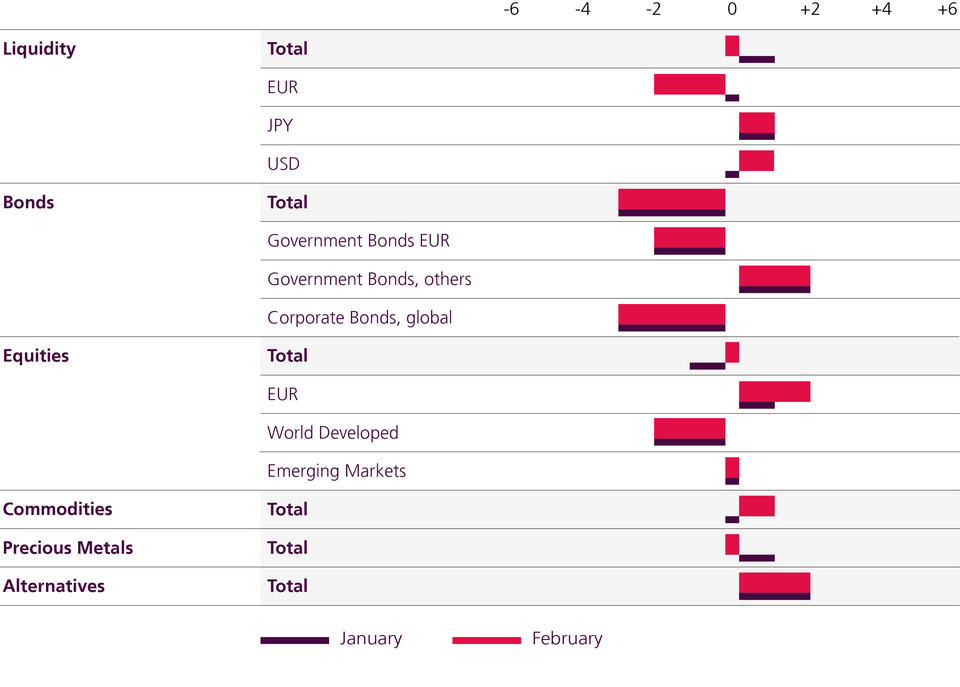

How do we position ourselves in February 2023?

We do not trust in this Goldilocks scenario quite yet. Valuations remain high for the ongoing slowdown in the economy and the prospect of interest rate cuts is too euphoric. However, as all major technical resistance has been broken and many investors continue to be defensive, we remain on the sidelines for the time being and are currently maintaining a neutral equity allocation. We remain underweight in CHF bonds and corporate bonds, and overweight in emerging market bonds. We anticipate outperformance in alternative investments. In equities; Europe and Australia remain our favourites.

- Commodity prices, especially energy, have not yet benefited from the reopening of China. This is likely to change soon.

- Natural gas prices have collapsed by more than 80% due to the warm weather, but this now seems excessive, not least because demand for gas will increase.

- Commodities remain a hedge if inflation should remain higher than currently anticipated for longer.

- Gold has gained 20% since November and is only 6% below the peak of March 2022.

- At that time, US real yields were -1%; now they are +1%. Geopolitical risks were highest with the outbreak of war in March.

- Since the USD could rise again after heavy losses, we are taking the profits made in gold.

- After a pronounced outperformance of +15% in 2022, the lead of health care is now fading away and the character of the sector is too defensive in the current environment.

- The valuation is too high for both health care (P/E > 20) and the SPI (P/E 18). At +14% for 2023, earnings expectations for Switzerland are also too euphoric.

- We are reducing pharmaceutical and Swiss equities, in return raising our existing preference for European dividend-paying stocks (including the UK). We like securities in the consumer sector, such as Unilever.

Asset Allocation Spezialmandate