The bear is waking up from hibernation

The bulls and bears are currently engaged in fierce battle. We have watched neutrally so far. However, we are now looking towards the bear side, as the currently priced-in Goldilocks scenario with a positive economy, low inflation and interest rate cuts seems far too optimistic to us.

Text: Stefano Zoffoli

The bulls emphasise that the economic figures have improved significantly and that a recession has now become less likely, meaning investors have to abandon their defensive stance. The bears see the risk of more persistent inflation in the robust economic figures and thus continued restrictive central banks.

At the same time, a number of indicators that we continuously measure provide a sell signal:

- the euphoria among retail investors is dangerously high.

- Financial conditions are beginning to turn again after considerable easing. The money supply and balance sheets of the central banks are declining significantly.

- At only 2.4%, the risk premium of equities against bonds is very poor and in the last 20 years was only similarly low before the financial crisis.

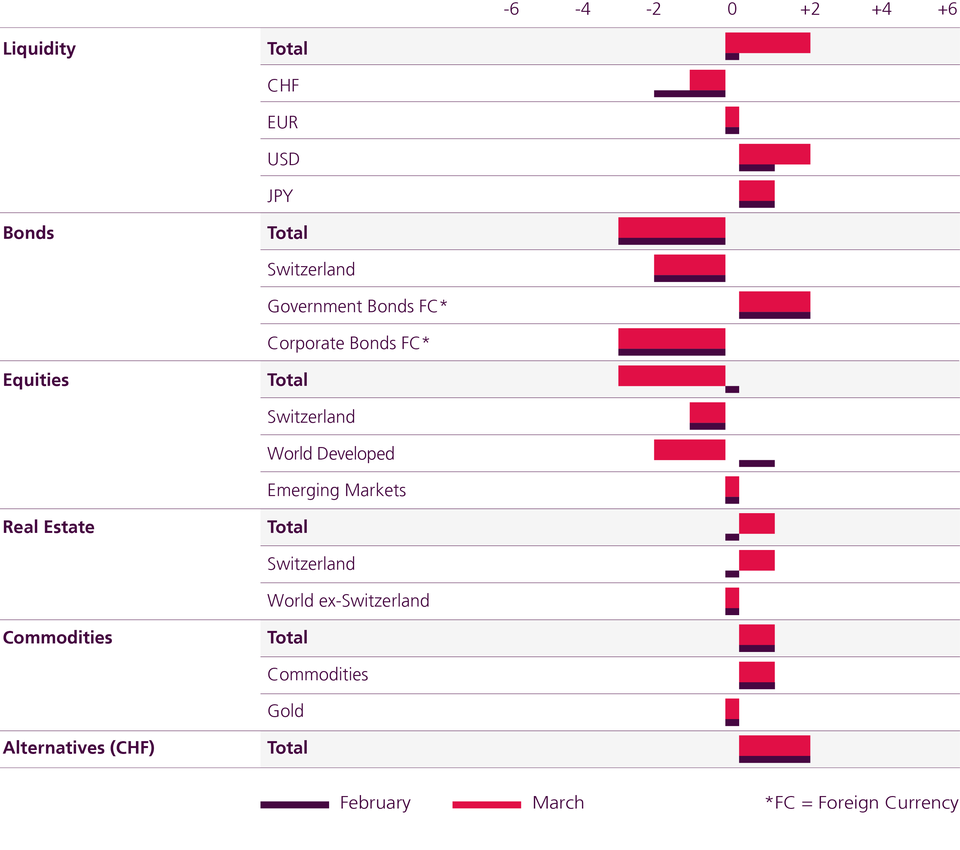

We are therefore underweighting equities and are currently preferring to invest in attractively valued alternative investments such as commodities, real estate and catastrophe bonds. In terms of bonds, we continue to favour US and emerging market government bonds over corporate bonds and European government bonds.

- European equities continue to be favourably valued in spite of their significant increase of 30% over the past four months. Their P/E is 13.0 compared to 18.5 for US and Swiss equities.

- We prefer companies with solid balance sheets, low debt and a high dividend yield.

- Companies such as Unilever, Ahold or the ING Group should perform better than expensive US large caps or Swiss equities in the current environment.

- Australian equities have been highly popular due to the strong relative earnings growth in view of the upturn in the Chinese sales market and the good price momentum.

- Now these factors are weakening and Australia is likely to slide into recession this year.

- In addition, as the major Australian banks are already making provisions for mortgage loans, we are taking profits here.

- Catastrophe bonds currently offer a historically high risk premium with a yield of around 10%.

- Premiums on listed real estate funds (5% on average) have rarely been lower in the last 20 years. Switzerland is experiencing a housing shortage – and this trend is on the rise.

- Commodities: The price of natural gas has fallen from an all-time high to an all-time low within six months, which now seems excessive. Other important contracts are also characterised by scarcity.

Tactical Asset Allocation March 2023