A Quantum of Solace: The Return of the Yield

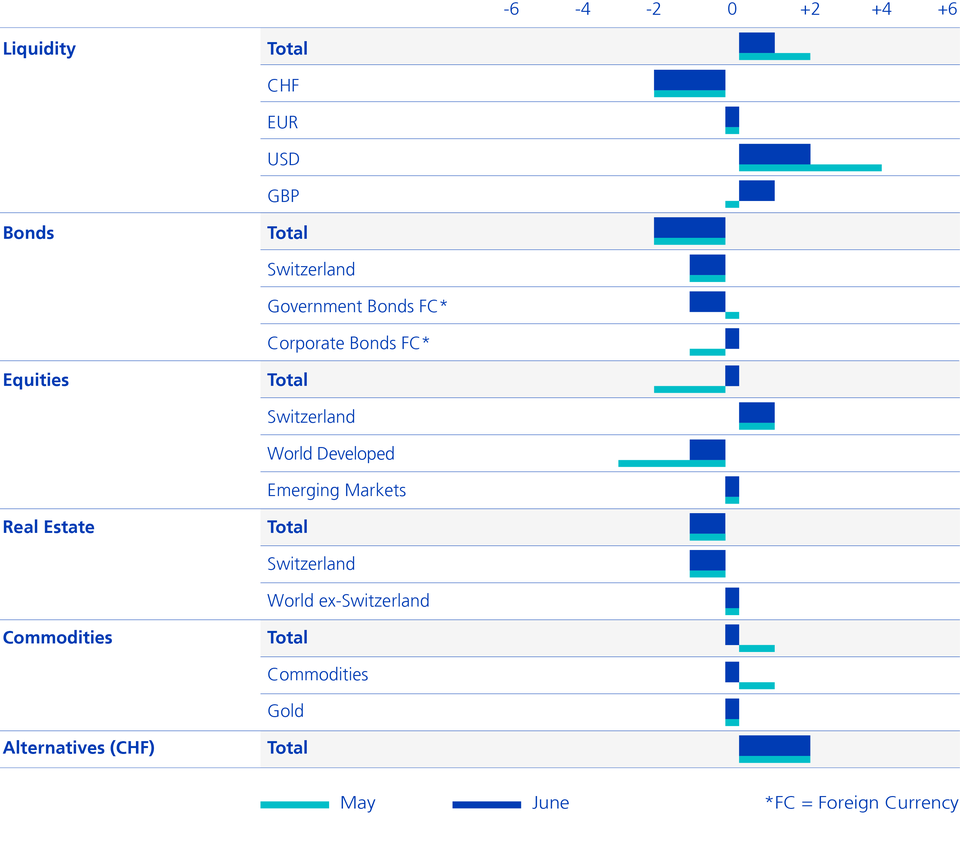

In general, we are reducing the tracking error in June after having performed very well so far with the underweight in duration, equities and corporate bonds and the overweight in commodities. For bond investors, there is some consolation after the sharp losses (-10% YtD): the earnings prospects are now significantly better than they have been.

Text: Stefano Zoffoli

Although inflation rates and bond yields did not increase further in May, global equity markets had to suffer another setback (-5%). With around 17% losses since the start of the year, global equities are standing on the brink of a bear market (20%). For a Swiss investor, equity losses are somewhat less dramatic thanks to the 11% appreciation of the US dollar.

According to a survey, fund managers are underweight in equities on average and cash levels are at their highest level in 20 years. Equity markets are already pricing in a slump in the economy; the US PMI, on the other hand, currently expects further solid growth at 55. The global economy also seems to be robust so far. Certain indicators, such as the German ZEW index, are in the process of moving upwards again.

If inflation actually falls as expected, the pressure on central banks is likely to ease somewhat and the likelihood of a soft landing will increase. This combination could provide for positive equity markets in the second half of the year – which is why we have closed our equity underweight. The downside risks are currently still too high for an equity overweight. We are also keeping the duration of our portfolios close to the benchmark after ending the underweight we have had since the start of the year.

- After more than two and a half years, we are now closing our underweight in corporate bonds.

- Following sharp losses (-14% over 1 year), spreads on government bonds are now above average again at 1.6% and at a similar level to Q4 2018.

- At 3.7%, the yield to maturity is now attractive again and significantly higher than the dividend yield on global equities (2.1%).

- The net gearing ratio has been reduced (currently still 3x) and interest coverage (profit/interest costs) is extremely high at 6x.

- The Canadian stock market has benefited from high energy prices; we are now taking part of the profits off the table because energy prices have less potential and the major financial sector (30%) could suffer from the weakening of the real estate market.

- On the other hand, we are once again building up European equity securities, including defensive telecoms and utilities.

- The price losses of recent months have revealed European companies from other sectors such as IT and cyclical consumption with high dividends.

- Commodity prices continue to be at an all-time high and the focus is on supply concerns due to bottlenecks and the war.

- Increased recession risks could lead to growing concerns about demand; industrial metals have already corrected significantly (-25%).

- In the past, high rolling returns were observed after around one year of reverting to the mean. This could be the case again. Higher interest rates also increase storage costs.

- We are therefore collecting the high profits (+33% since the beginning of the year) and reducing commodities back to a neutral position.

Asset Allocation Multi Asset Solutions

Our investment tactics of the past months

Tactical Asset Allocation May 2022

Tactical Asset Allocation April 2022

Tactical Asset Allocation March 2022