The euphoria is rather premature

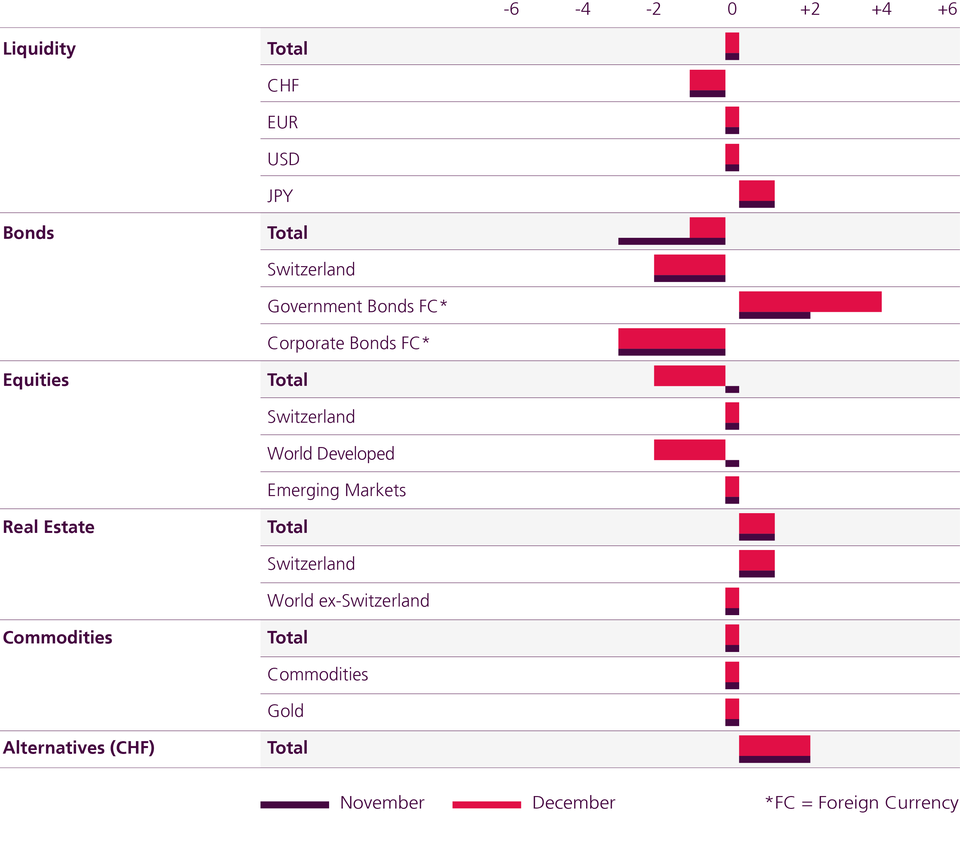

There is a short-term risk of a setback on the equity markets. This is why we are once again reducing the equity exposure below the benchmark. On the other hand, we are extending the duration of bonds with attractive yields in order to profit from falling inflation and an economic slowdown.

Text: Stefano Zoffoli

These are our reasons for reducing the equity quota:

- We believe that the hopes for a less restrictive monetary policy by the Fed from 14 December are premature.

- The increase in equity markets still lacks breadth, so it is likely to fail on the moving 200-day average in line with the two bear market rallies in March and July/August.

- The earnings estimates priced in by the market are too high at around 8% for 2023 and need to be reduced in the coming weeks or months, maybe to zero earnings growth.

With the price increase of the last two months, the momentum of investments with risk premiums such as equities and high-yield bonds has improved significantly. What's more, December exhibits historically strong seasonality, and inflation will continue to fall according to our forecasts, especially in the USA – from the current 7.7% to below 4% in 12 months. If, according to our estimates, the global economy weakens only mildly (global GDP in 2023: +1.6% after +2.9% in 2022), these are reasonable prospects for 2023. Growth for Switzerland is forecast at +1.0% after +2.5%.

- European banks and insurance companies – sectors with high distributions – are benefiting from the normalisation of interest rates and have their credit risks under control.

- Companies with high dividends continue to be cheap, both historically and compared to the overall market. Europe is still avoided by global investors.

- In the case of dividend futures, we believe that there is a risk that governments will make claims to extraordinary profits.

- The market is shifting its focus from inflation towards recession, especially in the biggest economy, the US. The USD yield curve is moving downwards in the medium maturity range and thus enabling price gains.

- We are maintaining our positions in inflation-protected bonds, which already compensate for inflation rates that are already too low, as well as ultra-long maturities of over 20 years.

- Overall, we are reducing the USD ratio in the portfolio because the USD interest rate advantage compared to other currencies has peaked and will gradually decline.

Asset Allocation November 2022