Hawks create new investment opportunities

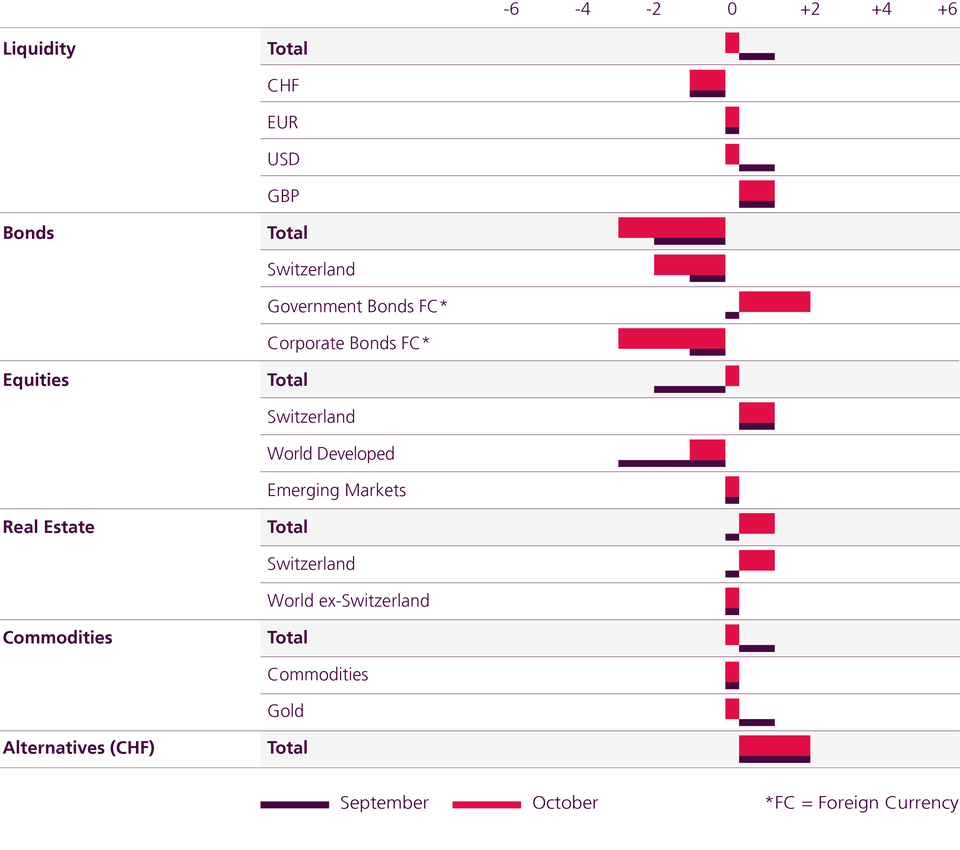

Let's take something positive out of this market situation! The 10-year bond yields are now already listed at around 4% in several countries (USA, Italy, UK and Australia). The TINA era ("There Is No Alternative" – to equities) seems to be definitively coming to an end. We are taking advantage of the attractive yield levels and are overweighting global government bonds; we are also reducing CHF bonds. Equities are oversold – we are closing our underweight.

Text: Stefano Zoffoli

It is surprising how reliably the stock market indicator of "seasonality" has again worked during September. We had warned about the seasonally weak equity months of August and September and indeed the equity markets lost another 12%. Of course, this was not only due to seasonality. The fundamental trigger for the correction was a steady rise in bond yields due to the continued surprisingly high inflation figures, for example in the US with 8.3% and 6.3% core inflation. In the UK, the new government is torpedoing the monetary tightening of the Bank of England with tax cuts.

We are increasing our underweight in corporate bonds because we consider the current spread levels, for example the 150 basis points in USD investment grade, and the associated implicit default rates to be too low in view of the increased recession risks. Last month, our equity underweight was justified on the basis that we had rated notions of interest rate cuts and high earnings expectations as unrealistic. We were right to do so. Today, significantly higher key interest rates and no interest rate cuts are expected; earnings expectations have been revised downwards slightly. In addition, as equity markets are now oversold with a relative strength index at 24 and less than 5% of US equities are trading above their 50-day average, we are closing our equity underweight.

- After the enormous losses of minus 14% YtD, yields on US government bonds at various maturities are close to 4%.

- The risks of recession are increasing due to the aggressive interest rate policy on the part of the central banks. We are therefore buying government bonds and we expect yields to fall slightly.

- The inflation expectations priced into the TIPS are at 2.2% across practically all maturities, meaning that fears of inflation have been fully priced out.

- In addition to nominal government bonds, we are therefore also buying US TIPS.

- After the biggest monthly loss of all time (-7.4% in September; -20% YtD), the average premium is only 8% and thus at the lowest level since the financial crisis.

- Despite the rise in interest rates, interest rates are currently still significantly below the discount factors for real estate (approx. 3%); no valuation corrections are pending.

- The current premiums imply a decline in the value of real estate of approx. 10%. We consider this to be significantly exaggerated.

- We have therefore purchased real estate funds and are now overweighted.

- The euro has lost more than 21% against the US dollar since the beginning of 2021 because the Fed has raised interest rates significantly more aggressively and earlier than the ECB.

- European pessimism is now extremely high with worries of a recession, the energy crisis and war. Positive surprises are more likely again.

- The ECB could replace the Fed as a hawkish central bank; a temporary rebound of the euro seems possible.

- We are closing our underweight in the euro and reducing our US dollar liquidity.

Asset Allocation October 2022

Our investment tactics in recent months

September 2022: Central banks knock down investors again

July 2022: Peak in inflation is still to come

June 2022: A Quantum of Solace: The Return of the Yield

May 2022: Stay short in May, but don't go away!

April 2022: Equities - Headwind expected again after recovery rally